Price Only Matters When You Sell For Cash

Price Only Matters When You Sell For Cash

“Nowadays people know the price of everything and the value of nothing.”

“Nowadays people know the price of everything and the value of nothing.”

Lord Henry, The Picture of Dorian Gray by Oscar Wilde

Founders and CEOs…Congratulations on raising your recent round.

Great news — the price per share that the venture capital funds just paid for the new round of preferred stock is higher than the price per share paid in the last round. The investors in your latest round believe that the company is moving in the right direction and, with continued strong performance, will provide them with a good return on their investment.

You and your communications team will want to talk about the fundraising amount and the implied valuation in a press release, potentially in press interviews and definitely in the All Hands meeting with employees.

My advice: don’t get attached to this implied private market value. It means very little.

One venture capital firm, who “led” the round, set the price per share. Usually, that firm has offered the highest price per share, if there were multiple bidders who submitted term sheets. Or they may have been the only investor who provided a term sheet at the price you and your Board found acceptable.

This investor set a “market clearing price”. The price is “offered” at a single moment in time. The investor has not accurately determined the “fair value” of you company. The price for your shares can and will change, daily if a market existed, and certainly over time. The new investor also acquired preferred stock, which is different from the common stock that management and employees own or can buy. I touched on that important distinction in an earlier post. In brief, preferred stock is always worth more than the common stock due to its special rights and protections.

Fair value is an intrinsic measure based on the actual and expected future performance of the company — future financial performance expectations don’t typically change all that frequently. Having multiple parties examine detailed market, financial, and operating data over time helps determine fair value. This is what public markets do over the long term. As the legendary value investor Benjamin Graham said: In the short run, the market is a voting machine but in the long run, it is a weighing machine.” By voting machine, he meant something akin to a popularity contest. This bias towards popularity is exacerbated in private market transactions, when the “winner” in the bidding for the right to invest had to be the most bullish on the potential of the business. And thus the winner offers the highest price per share. This private investor may or may not be right about the long term value of the business.

In private market transactions, price per share really only matters when you sell for cash. Cash outs are rare in private investment rounds. Sometimes, founders and early investors do sell a part of their ownership in the investment round (this sale of existing shares is called a “secondary” transaction). When existing founder CEOs sell a part of their ownership, it is likely a small piece — they will typically maintain the majority of their prior ownership. Investors want existing management (especially the CEO and other founders still involved in running the business) to have meaningful financial upside potential tied up in the business. In this way, management’s financial incentives are aligned with the investors — both parties having future wealth creation linked to company performance.

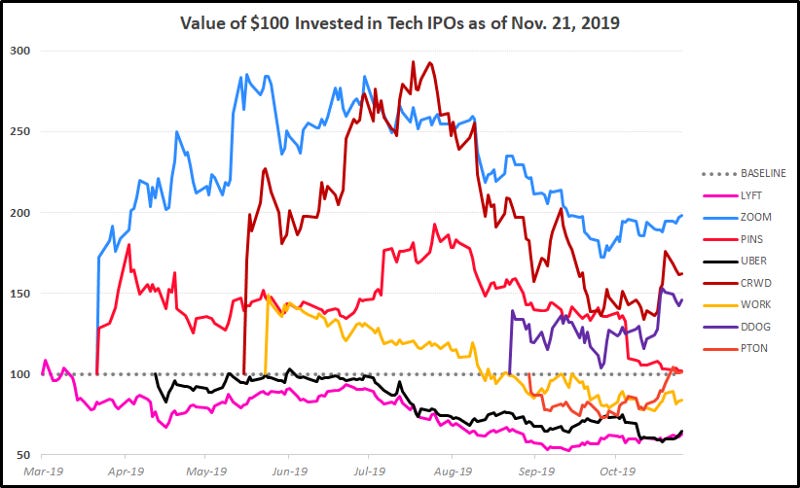

Even in a traditional IPO, management does not typically sell their shares until at least 180 days after the public listing (that length of time is called the “lock-up period”). And even then management usually only sells a portion of their holdings. Senior managers (especially the CEO) are advised to maintain ownership post IPO. Why? Because their selling stock in large quantities would signal to other investors (institutions or individuals who know less about the business and its prospects) that this level is the highest the stock price will reach, at least for the near future, thus putting downward pressure on the stock price. Press reports on IPOs generally talk about how the stock traded on the day of the IPO but rarely track performance thereafter. A lot can happen to the stock price in a 180 days from the IPO — look at the stock performance of major tech IPOs of 2019 (shown below, indexed to the IPO price).

The straight line up on several IPOs represents the first day “pop” in the price.

Another path to getting cash is to sell your business — the financial world calls these transactions, M&A (mergers and acquisitions). Even M&A events are often structured as stock swaps (the seller exchanges their company stock for the stock of the acquiring company) or a mix of cash and stock rather than a 100% cash payment. The recent travails of WeWork offer an insight into how private market M&A valuations may not be as lucrative as they seem on the day the transaction is announced. Managed by Q (a company helping office managers deal with supplies, cleaning, IT etc.) was acquired by WeWork in April 2019 (about 8 months ago) for a mix of cash and stock. Reports suggest Managed by Q shareholder received $100 million in cash and $120 million in WeWork preferred stock. The number of shares of WeWork preferred stock issued was based on the WeWork private market valuation as of April 2019. At that point WeWork’s private market valuation was $47 billion. Fast forward 8 months — current private market estimates of WeWork valuation are $8 to $15 billion. So Managed by Q shareholders today own WeWork stock that is worth up to 80% less than what they thought it was when the sale closed.

Founders and CEOs — don’t get too hung up on the valuation or price per share at which you raise money in the private market. The press and your peers usually obsess over this metric. Instead find the “right” investor, who besides providing capital, can help you grow/operate the business. And then, focus on building a great company which delights its customers, employees and investors.

The price per share only matters when you sell your stock for cash.