Moneyball for People: Finding “Hidden Gems” in the Hiring Process

“Startup [hiring] is simple. Either: 1) become among the best in the world at identifying mispriced assets, 2) convince incredible people…

“Startup [hiring] is simple. Either: 1) become among the best in the world at identifying mispriced assets, 2) convince incredible people to work for less, 3) pay top of market, or 4) build a mediocre team.

~everyone thinks they are doing 1/2; nearly everyone is actually doing 3/4.”

Zack Kanter (posted on Twitter on November 17, 2019)

This tweet caught my attention — I substituted “startup hiring” for what Zack wrote as “startup comp” in his original post as I believe it still captures his intent. I have spent the last 10 years of my career working at under-capitalized businesses and start-ups (both types had cash and thus spend limitations). So it has been critical to business success to attract prospective employees who are “hidden gems”. On pay alone, in a competitive auction for talent, we were unable to compete for talent with Amazon, Netflix or Salesforce (to name a few of companies to whom I’ve lost talent.)

I’ve been a fan of Michael Lewis’ writing for a long time and was particularly fascinated by Moneyball. While the details of the book are about baseball, the principle it addresses is how an under-capitalized organization (in his case the Oakland Athletics around the year 2000) could compete with much wealthier opponents (the Yankees, RedSox and Dodgers) and have success beyond what would be expected given their financial means. The insight Lewis offered was that the A’s General Manager, Billy Beane, who led the talent evaluation and acquisition function at the organization, focused on what he deemed “mispriced assets”, players who did not rank high based on the rubric for evaluating talent that other organizations were using, but in whom he saw higher value.

All venture investors will tell you the team is very important to their investing decision. And the importance increases when the investment is in an earlier stage business. For seed and even A round investments, investors place a significant weight on the ability of the CEO/founding team to recruit exceptional people and bring them onboard at below market compensation. This approach is what Zack refers to as #2 above.

My experience is that this approach doesn’t scale once a company has been in business for a few years and the number of employees has grown to above 50. At that point many employees realize, particularly if there have been ups and downs in performance as there are in most companies, that they’re part of a “business” and deserve to be paid market value for their skills.

At some point in the hiring funnel, the recruiter and hiring manager narrow the pool of potential candidates based on their match against a desired psychological profile (values, attitudes, beliefs etc.) and ideal skill set. Assuming the candidates perform broadly in line with their skills and background in interviews and skills tests, once the pool is narrowed, hiring, like all other capital allocation decisions, is principally an investment decision.

In the investment decision phase of hiring, the hiring manager selects the new hire from a short list of potential candidates — she is the individual whom is expected to generate the most value over their tenure relative to their cost. And both the interest in this candidate and the willingness to pay them is based on this forecast of estimated future contribution to the business.

When I suggest hiring is an investment decision, many people find that approach dehumanizing — they may think, “is it reasonable to convert a hiring decision into a discounted cash flow analysis?” The reality is most of us often do that type of mathematical calculation in our heads in other ways. When presenting our case for a new hire to our manager or the People Operations department, we make some mixture of the following arguments. I need additional resources (employees or consultants) to either: (a) grow revenue directly; (b) grow revenue indirectly by increasing customer satisfaction which will lead to renewal, upsell, additional purchases, referral or improved brand value; (c) reduce cost; or, (d) reduce risk or complete a necessary compliance task.

For a relatively “known” new hire, growing tech companies or tech-enabled companies that have revenues below $100 million and not profitable yet (which describes a huge pool of potential employers) can rarely rationally offer the same guaranteed compensation as a larger public entity with a similar business model (e.g. Facebook, Google, Amazon, Salesforce). I’ve put the word “known” in inverted commas because when there is a narrow range of expected future performance, then larger, more established employers will always be able to offer a higher compensation package.

The accepted way to calculate the net present value of a new project or investment is to discount back the expected future cash flows at the appropriate cost of capital (a measure of risk-adjusted return expectations). The net present value represents the ceiling that one should be rationally willing to pay. The appropriate cost of capital is a critical input as it will dramatically change the net present value.

Larger, profitable growing companies have a lower cost of capital than smaller, unprofitable but promising (venture-backed) businesses. Large companies have a lower cost of capital because they have proven then can meet their own forecasts for future performance and create value. Thus they attract investors (debt holders and public equity owners) who demand a lower rate of return knowing the risk they are taking on future performance is lower. In addition larger companies can take greater risk because their cushion (cash on hand to offset a bad outcome) is much greater, and thus can either overpay compared with expected value for a single hire.

When a candidate has multiple job offers, and the different businesses vying for her services have similar expectations on future performance, then the business with the lowest cost of capital (typically a larger company, often publicly traded and profitable) can afford to pay more for their services than the competing firms.

So most venture-backed businesses or family-owned businesses need to hire on the basis of identifying and taking risks on what they believe are mispriced assets or hidden gems.

So how does one identify mispriced assets. It is really hard. If it were easy everyone would be doing this and the inefficiency (excess return potential) would disappear leaving no mispriced assets. Warren Buffet’s mantra on investing applies to hiring: “Investing is simple, but not easy.”

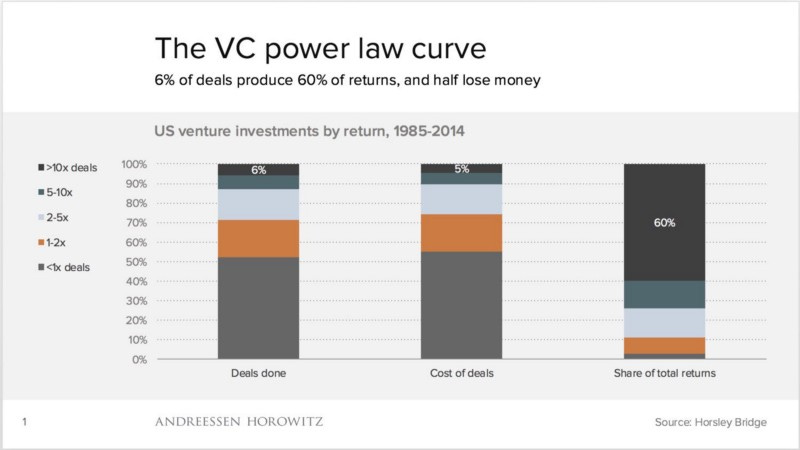

To find mispriced assets, you have to be willing to be wrong. Professional venture capital investors know this all too well. The graph below, recently retweeted by Benedict Evans, speaks to how venture investors must accept a significant risk of failure in a quest to find exceptional investments.

The same truth applies to hiring, especially at start-ups. So looking for mispriced gems is not without risk.

Howard Marks, an investment expert whose periodic memos I look forward to, posted an excerpt from Chapter 1 of his book The Most Important Thing in his September 2015 memo entitled It’s Not Easy. I substitute in his quote below “building a business” for “investing”, “business builders’’ for “investors” and “business” for “investment.”

“Remember, your goal in [building a business] isn’t to earn average returns; you want to do better than average. Thus, your thinking has to be better than that of others — both more powerful and at a higher level. Since other [business builders] may be smart, well-informed and highly computerized, you must find an edge they don’t have. You must think of something they haven’t thought of, see things they miss or bring insight they don’t possess. You have to react differently and behave differently. In short, being right may be a necessary condition for [business] success, but it won’t be sufficient. You must be more right than others…which by definition means your thinking has to be different….”

Below are my thoughts on finding, hiring and realizing value from hidden gems (things that look like coal but can be transformed into diamonds.) I welcome input on other tactics that you have found helpful.

Look Where the Crowds Aren’t Looking: In the hiring world this may take the form of considering those who are either under or over qualified on paper. Or it may mean going outside the conventional age range for the role.

Be Aware of Your Subconscious Bias which will Draw you to Conventional Credentials: Whether we like to admit it or not, we all look for credentials in evaluating resumes. These include university record (name, degree and GPA) and past jobs (looking for brand name employers). A former colleague of mine shared his approach to hiring sales people. And that wisdom has stuck with me. He talked about seeking out people who had prior sales experience at relatively unknown businesses and still managed to perform reasonably well against their quota metrics. If you are capable at having success selling a less known solution provided by a no-name business (and not just be a successful salesperson at Slack or Salesforce), you are more likely to do well in a new role.

Be Careful of an Over Reliance on the “Eye Test”: The most frequently discussed example of this is the performance by Tom Brady at the 2000 NFL combine (video here) which in part led to him being selected in the 6th round of the draft. With 20/20 hindsight, the “eye test” was way off. In the professional world, the eye test often takes the form of evaluating people on their spoken English (even when it is not their first language) or assigning a high correlation between extraversion or people-skills and future job success.

Offer Recruiters The Opportunity to Go Outside The Hiring Specification: Good, experienced recruiters develop a “gut feel” about people they talk with which cannot be easily quantified in a resume. While you as the hiring manager may have a lot of confidence in the correlation between a particular profile and future role success, encourage the recruiter to bring you people they really like outside your core specification.

Look for Internal Candidates from Other Departments: These people already know your business. They may have hit a ceiling in their current role for a variety of reasons or may simply be looking for a different growth opportunity. A lot of the “culture fit” risk doesn’t exist with internal candidates. Reducing the risk around culture fit, not having to teach the candidate as much about the business, and avoiding the cost of hiring can more than offset the risk of the candidate not having the ideal background and skill set.

Seek Out “Fallen Stars”: Fallen stars can mean a lot of different things. Some that come to my mind include those who have left the W-2 full-time workforce for an extended period of time — it might be for any number of reasons including: (a) to raise children; (b) to care for an ailing relative; © to deal with a personal mental/emotional health issue; or, (d) to start their own business. We overvalue the signal candidates provide by simply having a current job. In this era of job mobility and flexibility, don’t discount those who appear to have taken a different route compared with the accepted linear career path.

Screen for Curiosity and Interest in Learning: I find a subtle, yet very important difference between people who strive for success and strive for learning. We all want to be successful at what we do, and yet those of us who are self-aware know we will fail a lot. So I try to seek out those who are both interested in learning and willing to admit they don’t know how to do everything. Ask how people have tackled learning challenges, especially in unstructured environments, and listen to how they answer the question, looking for internal motivation and drive.

Look Outside Your Industry Vertical: Employers tend to over-value prior industry experience. I find it amusing and sad that most non-profit roles actively discourage anyone without a non-profit background from applying for senior roles. There is a lot more in common across different types of businesses that most employers realize as they have myopically focused on solving problems in one industry for an extended period of time. In fact, generalists, who are skilled at pattern matching across industries, will typically bring a very valuable, fresh perspective to your organization.

Ask Candidates to Talk About Failure and What They Learned From That Experience: The general advice around interviews is to exude confidence and talk about all your successes. Test if candidates are willing to talk about failure. And particularly, what they learned from that experience of failure. To reduce the pressure on the candidate, normalize that failure is common, make it clear you are focused on the learning and unconcerned about the failure itself.

Tell Candidates About the Bad Parts of the Job Relatively Early in the Interview Process: Hiring is a process fraught with lack of trust. Some of the key questions candidates are trying to figure out in an interview include: “What is this job really like?” and “Can I trust my boss?” So, being upfront about the bad parts of the job — every job has elements that are boring, repetitive, challenging etc. — signals you are trustworthy. Trust helps a ton with hiring and retaining great people.

Be Clear the Company Offers “Rewards” Other than Money: If you offer a fair wage (not top of market) for the role and experience level of the candidate, the people whom you really want to hire will realize that an incremental $5000 or $10000 in pay is less important than other non-monetary factors. Speak to a combination of psychological/emotional rewards you will offer (public recognition, ability to speak in front of the leadership team, whole company, at a conference etc.) and intellectual rewards (training, development etc.) during the hiring process. And follow through on these promises; they will have a self-reinforcing effect on your brand.

Always Keep Developing People and Offer Them Opportunities to Learn: Experience (past roles, employers, industry) is put on a resume for everyone to see. Often it is overvalued when evaluating candidates. So when looking for hidden gems, offer them learning and development on a continuous basis — within their specialty/role, in adjacent roles and in totally separate departments. The “right” candidate will find this type of opportunity invigorating.

Finding mispriced assets doesn’t mean you pay them below their market value forever. Rather just that you hire them because you see something in them that others don’t (the diamond rather than the coal) and offer them something that other’s are unwilling to do, such as training or the opportunity to prove themselves. Eventually you need to pay a fair wage to retain and motivate people. Everyone wants to feel valued.

Charlie Munger (Warren Buffet’s longtime partner) has a “no-bs approach” to sharing his wisdom. He told Howard Marks over lunch in 2011 something about investing which applies equally well to hiring, especially when looking for mispriced assets:

“It’s not supposed to be easy. Anyone who finds it easy is stupid.”