Capital Efficiency — Part I

Capital Efficiency — Part I

As the pendulum shifts from growth at all costs to growth balanced with efficiency, I offer some thoughts on efficiency metrics.

As the pendulum shifts from growth at all costs to growth balanced with efficiency, I offer some thoughts on efficiency metrics.

“Never spend your money before you have earned it”.

- Thomas Jefferson

Venture capitalists, angel investors, bankers, and consultants write and talk about the key metrics that matter in evaluating the attractiveness of a business. During much of the ongoing bull market for public equities, which is now in its 11th year, the focus has been on revenue growth and customer growth. My favorite description of the world we’ve lived in for the last several years (particularly applicable to tech-enabled start-ups targeting consumers) is from residential real estate expert Mike DelPrete. He said that the favored business model of the last half-decade is “the competitive advantage of sustained unprofitability, subsidized by venture capital” (I am slightly paraphrasing his words here).

Since early October 2019, following the failure of WeWork to go public, the drumbeat on the importance of profitability and sustainable business models has been growing. And on February 5th of Casper Sleep entered the public markets at below half of its last private round valuation set less than a year ago in March 2019. These negative public market reception of these two household names will increase further, especially around consumer-facing, tech-enabled businesses, the focus on profitability and free cash flow.

In case you missed the articles in the mainstream press and tech press about the need to re-weight the relative importance of growth and profitability, here are a few links to pieces that ran in the New York Times, the Wall Street Journal and TechCrunch. To me, the most unintentionally ironic statement was by the CEO of Bird, the largest e-scooter company, who said, in a statement e-mailed to all employees accompanying a large fundraising round announced in early October 2020: “Positive unit economics is the new goal line.”

So are we entering an era where efficiency is really almost as important as growth and where burn rates matter?. It’s hard to say. I do recall many venture investors and operators had that feeling in Q1 2016 when both LinkedIn and Tableau Software stocks dropped by almost 50% in a single trading day. And yet in a few months, the focus on growth at all costs returned.

My traditional finance training has always led me to look for businesses (to invest my time and money) which can generate value efficiently. I think about this concept slightly differently from most of the venture capital community.

When venture capital and growth equity investors talk about efficiency they tend to focus on some mix of the following metrics:

(a) LTV to CAC ratio (thank you, David Skok, for the primer here);

(b) Unit Economics (a good explanation here); and,

(c) Magic Ratio or Magic Number (explained here);

A few will focus on

(i ) the Rule of 40 (explained here)

or

(ii) the Efficiency Score (a metric popularized by Bessemer Venture Partners as their version of the Rule of 40, and explained here in a thoughtful, albeit slightly dated piece);

The first three ratios relate sales and marketing spend to revenue and revenue increases. The latter two take into account total operating expenses and total cash burn respectively and so are better indicators of efficient use of capital.

All these ratios are marginal calculations — by “marginal” I mean, they describe what happened on an incremental basis with regard to a recent period. Experienced finance teams may track and thoughtful investors may ask to see the trends in these metrics over time to understand the direction they are moving in. For new potential investors marginal calculations, which inform them on the likely efficiency of future spend (their investment dollars), make a ton of sense.

However, for all the early investors in a business, including the founders and many early employees, the most relevant measure of efficiency is based on cumulative capital invested. Cumulative capital raised determines how much dilution founders, early employees, and early investors have taken. Furthermore, it is rare for a business that has not been efficient with capital raised in the past, to become more efficient with a new large round. So, where efficiency is concerned, I believe past performance is the best indicator of likely future performance. If you want to be convinced otherwise, I would recommend getting the CEO or CFO to lay out in detail how they will improve efficiency in COGS, customer acquisition or R&D without affecting the product or customer satisfaction. And then decide for yourself whether they can pull this off.

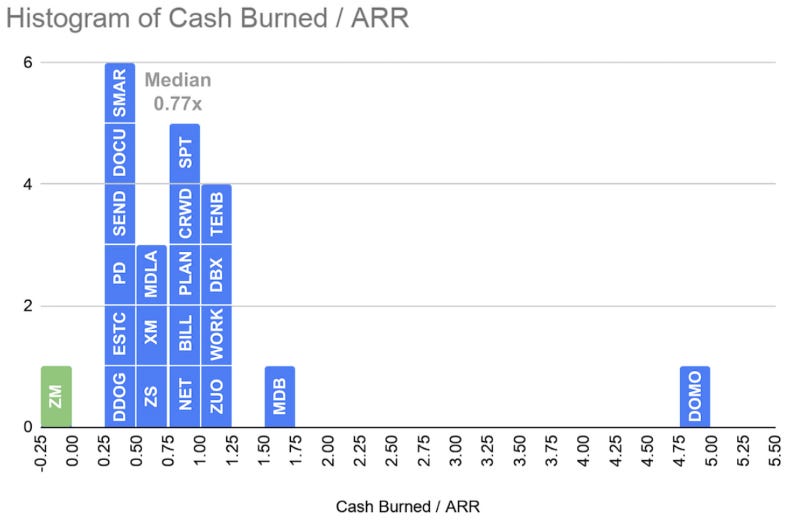

A few weeks ago, an interesting analysis was published by Shin Kim relating cumulative capital raised to revenue. His focus was on public SaaS companies driven by the availability of data. We should remember companies that get public are generally far better performers relative to the entire set of SaaS businesses. An interesting graph from that article is shown below.

I chose this graph to highlight as many of us may be able to do this analysis on private companies we work at. And if we are interviewing for senior enough roles, we should be able to get this data as part of our diligence process before accepting the job. He does note this metric has a high correlation with the Efficiency Score and Rule of 40 metrics described above.

This analysis focuses on SaaS business models. We can normalize this to other business models (B2C subscription, B2C e-commerce, marketplaces, etc.) by using run rate gross profit as the denominator. Given the average public SaaS company gross profit margin is around 75%, one can extrapolate that the median capital raised / run rate gross profit for SaaS companies would be ~1.03x. The correlation between this ratio and the valuation multiple of revenue is quite high, and thus a good proxy for how the company you work at or an interviewing with might be valued in a transaction.

So when trying to evaluate and compare businesses on capital efficiency, I would recommend using this metric (the ratio of cumulative cash consumed to annual gross profit). And, if possible to benchmark yourself, get the same data for your competitors and comparable companies with similar business models — your investors may be able to provide this on a no-name basis from their portfolio.

(Part 2 of this extended piece on capital efficiency will be published on February 12, 2020.)

The Capital

The latest Tweets from The Capital (@thecapital_io). The Capital is a financial micro-blogging social networking…twitter.com