A More Attractive Business Model for Tech-Enabled Consumer Product Companies

A More Attractive Business Model for Tech-Enabled Consumer Product Companies

“I’m building a business selling a high quality, hardware product to consumers which they love. I am seeking capital to scale the…

“I’m building a business selling a high quality, hardware product to consumers which they love. I am seeking capital to scale the business.”

These words will rarely get the hearts of investors or bankers fluttering with excitement. Start-ups pursuing hardware business models have a history of poor outcomes.

Since Marc Andreesen wrote “Why Software Is Eating The World” in August 2011, most venture investors have doubled down on investing in models that are software-centric or behave like software from a business model standpoint. These businesses are recurring revenue, high gross margin businesses that can achieve scale (>$100MM in revenue) efficiently.

Tech-enabled businesses selling to consumers, especially those leading with a hardware or physical product, are struggling in the public markets, particularly in the last 6 months. This wasn’t always the case. The public markets were receptive to high growth consumer tech businesses for a sizable part of the past decade.

(i) GoPro: Went public in June 2014 at $24/share and peaked at ~$98/share — today it trades below $4/share.

(ii) Fitbit: Went public in June 2015 at $20/share and reached at peak of ~$51/share — today it trades ~$6.50/share (~15% below the price recently offered by Google to buy the business.)

(iii) Sonos: Listed publicly in August 2018. Today, the company is almost break-even with expected revenue and EBITDA growth of 10% and 20% respectively. Today it trades almost 30% below the IPO price.

(iv) SmileDirectClub: Priced its IPO in September 2019 above the filing range at $23/share valuing the company at $9 billion which at the time represented a double digit multiple of revenue — today it trades below $7.50/share.

There is always an exception to every trend. The second most valuable company in the world — Apple — is at its core a consumer electronics business. Apple which boasts gross profit margins of ~40% (a level roughly in line with the gross margins of the other names mentioned above) is valued at ~5x revenues. The businesses named above are valued between 1x and 2x revenues. Apple gets a premium valuation as a result of its scale, consistent product excellence, strong brand and unparalleled customer loyalty.

In an effort to adapt to investor preferences of the “as-a-service” business model, consumer hardware businesses are working to add a recurring revenue component to their offering. Some offerings resemble financing plans with a committed upgrade path (Sonos is pursuing this avenue). Others are adding premium subscription offerings with data storage and a warranty (GoPro is taking this path) or personalized advice/coaching based on data (Fitbit premium). These are really “premium” add-on offerings which are likely to attract only a small portion of the product buyer universe. Put another way these are recurring revenue business model add-ons without a realistic path to a high attach rate and scale.

Over the last few quarters I have been hearing more about several “next generation” consumer product offerings that combine a hardware product with a higher margin recurring revenue service. The core offering (not a premium version) combines both these revenue streams. And both the hardware business and the recurring revenue component have attractive gross profit margin profiles.

Some people may say this is just the “razor and razor blade” business model followed recently by the likes of Keurig Green Mountain in coffee, Harry’s/Dollar Shave Club in grooming products, and Hewlett Packard with printer and ink cartridges. There are two key differences. In the “razor / razor blade” model, the base product is sold at a low price or given away for free (i.e. likely at a negative gross margin). And the “complementary” repeat purchase product is also hardware and not software/services.

The sector that is spawning the largest number of businesses adopting this “next generation” hardware model is the healthcare technology space — including both the OTC “medical device” segment as well as the fitness/wellness segment. Most of the companies (such Mirror or Tonal in the fitness space or several small and growing businesses in the hearing aid space) are privately held so their financial performance is unknown. The exception is Peloton.

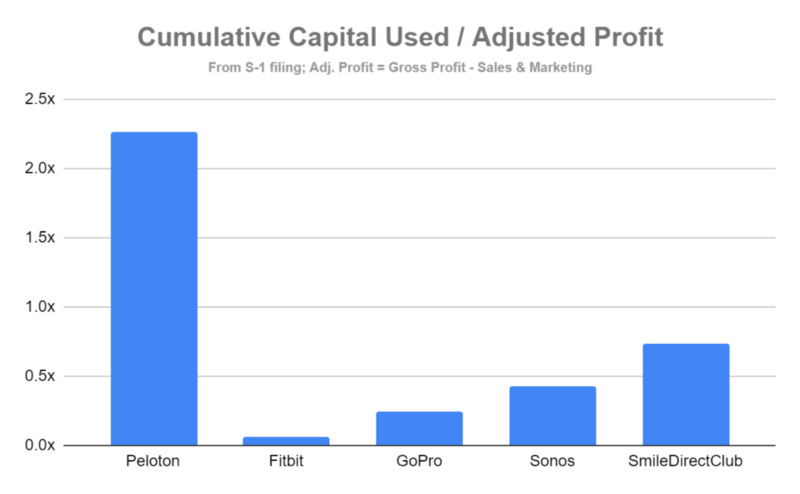

I have never used the product myself nor do I have any good friends who talk about it with me, so I was naturally a skeptic of their business model. At first blush, the business model seemed fairly capital intensive — Peloton had burned over $750 million prior to the public listing. Comparing it to the other well-known consumer products companies that have IPOd in the last decade, Peloton seems inefficient on the surface.

And yet its recent financial performance is fairly compelling and showcases how its combined profitable hardware + recurring revenue model represents the future for hardware centric businesses.

(i) Hardware Gross Margin:~40%

(ii) Recurring Revenue Gross Margin: ~57% (in Q1 2020) up substantially from the prior year.

(iii) Revenue Growth: ~75% yoy growth in consumers purchasing the produce.

(iv) Growing Engagement: all cohorts showing increasing usage / month in recent quarters.

(v) Efficient CAC: Perhaps the most important thing is that hardware gross profit almost entirely covers the entire sales & marketing spend.

(vi) Retention: Appears fairly strong for a consumer offering (this is perhaps the biggest wait and see area for me.)

→ Unit Economics are compelling

Not surprisingly, Peloton is one of the few consumer-facing IPOs to actually have traded up from its listing price. The other recent consumer IPO I can recall that has traded up is Chewy — while it is a retailer (a category that has fared extremely poorly given the overhang of Amazon), it focuses on the pet category which is somewhat unique. “Pet” is experiencing secular growth (similar to health/wellness) and many pet products (food, medications etc.) exhibit behavior similar to subscription products with regular re-order and low churn.

I expect to see more consumer hardware companies looking to launch similar business models to Peloton. And of course, I am curious to hear from all of you if you know of others in the public domain that I should look into.

(If you like this piece, please share my content with your friends and followers, and read other articles at https://medium.com/@adehejia.)